Inventory planning & control

A stock or store of goods

- The stored accumulation of material resources in a transformation system

- Allow the flexibility

- Exceptional quality

- Give a level of dependability

- Better return on investment (ROI)

Functions of Inventory

- To meet anticipated customer demand

- To smooth production requirements

- To protect against stock outs & take advantage of order cycles

- To hedge against price increases

- To permit operations

- To take advantage of quantity discounts

Types of inventory

- Buffer inventory (safety inventory)

- Purpose is to compensate for the unexpected fluctuations in supply & demand

- Cycle inventory

- One or more stages in the process can't supply all produced items simultaneously

- Decoupling Inventory

- Allows each operation to be set to the optimum processing speed

- Pipeline inventory

- Goods-in-transit to warehouses, distributors, or customers

- Raw materials & purchased parts

- Work-in-process (WIP)

- Finished-goods inventories

- Maintenance & repairs (MRO) inventory

Objectives of Inventory Control

Although inventory plays an important role, there are a

number of negative aspects

- Inventory ties up money, in the form of working capital

- Inventory incurs storage costs (leasing space, maintaining appropriate conditions)

- Inventory may become obsolete as alternatives become available

- Inventory can be damaged, or deteriorate

- Inventory could be lost, or be expensive to retrieve

- Inventory might be hazardous to store & require special facilities

- Inventory uses space that could be used to add value

- Inventory involves administrative & insurance costs

Inventory turnover: Ratio of average cost of goods

sold to average inventory investment

- A widely used performance measures to judge the effectiveness of inventory management

Requirements for effective inventory management

Management has two basic functions concerning inventory

- To establish a system to keep track of items in inventory

- To make decisions about how much & when to order

- A system to keep track of the inventory on hand & on order

- A reliable forecast of demand that includes an indication of possible forecast error

- Knowledge of lead times & lead time variability

- Reasonable estimates of inventory holding costs, ordering costs, & shortage costs

- A classification system for inventory items

Inventory Counting Systems

- Periodic system: Physical count of items in inventory made at periodic intervals (weekly, monthly)

- Perpetual inventory system: Keeps track of removals from inventory continuously, thus monitoring current levels of each item

- Two-bin system: Two containers of inventory; reorder when the first is empty

Inventory Costs

Basic costs which associated with inventories are as follows

- Purchase cost

- The amount paid to buy the inventory

- Holding or carrying cost

- Cost to carry an item in inventory for a length of time, usually a year

- Transaction or ordering cost

- Costs of ordering & receiving inventory

- Setup costs

- The costs involved in preparing equipment for a job

- Shortage cost

- Costs resulting when demand exceeds the supply of inventory; often unrealized profit per unit

- Obsolescence costs

- There is a risk that the items might either become obsolete (change in fashion) or deteriorate with age (foodstuffs)

Inventory priorities ( ABC system)

Classifying inventory according to some measure of

importance (usually annual dollar value), & allocating control efforts

accordingly

Typically, three classes of items are used

- A (very important), B (moderately important), & C (least important)

A item generally (10-20) % of total inventory but (60-70) %

of total annual dollar value

On the other hand, C item might account about (50-60) %

total inventory but only about (10-15) % of the dollar value of an inventory

cost.

These percentages vary from firm to firm

Steps to solve an A-B-C problem

- For each item, multiply annual volume by unit price to get the annual dollar value

- Arrange annual dollar values in descending order

- The few (10-15)% with the highest annual dollar value are A items. The most about 50% with the lowest annual dollar value are C items. Those in between about 35% are B items

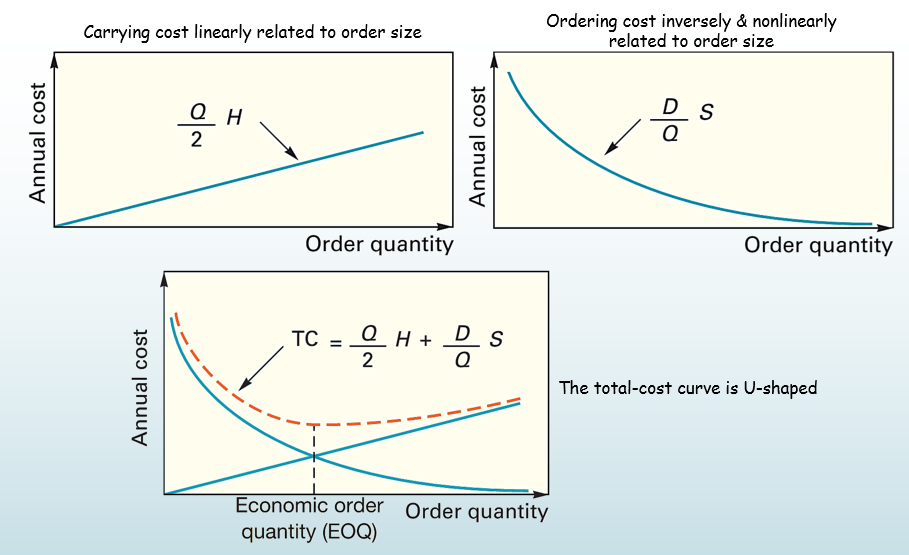

Economic order quantity (EOQ)

The order size that minimizes total annual cost

- Find the best balance between the advantages & disadvantages of holding stock

- Find a fixed order size that minimize annual cost of holding & ordering inventory

Holding costs are including

- Working capital costs

- Storage costs

- Obsolescence risk costs

Order costs are including

- Cost of placing the order

- Price discount costs

Reorder point (ROP)

When the quantity on hand of an item drops to this amount,

the item is reordered

ROP = d × LT (Where, d = demand rate & LT = Lead time in days or weeks)

Safety stock: Stock that is held in excess of

expected demand due to variable demand &/or lead time

Safety stock reduces risk of stock out during lead time

Determinants of the reorder point quantity

- The rate of demand (based on a forecast)

- The lead time

- The degree of stock out risk acceptable to management

- The extent of demand &/or lead time variability

No comments:

Post a Comment